Whirring machinery and humming conveyor belts are no longer the only mechanical sounds heard throughout the modern warehouse or DC operation, where the rise of robotics is transforming the industry and helping companies improve efficiency, accuracy and productivity.

And because automatic guided vehicles (AGVs), articulated robots and collaborative robots (cobots) work tirelessly—in some cases even around the clock—they’re also helping companies cure an ill they’ve been grappling with for years: the warehouse worker shortage.

To gauge how companies are using and plan to use robotics in their operations, Peerless Research Group partnered with MHI and The Robotics Group to produce the third annual Intralogistics Survey. A lot has changed since the survey was first conducted in 2022, at which point many companies were just beginning to test the waters of intralogistics robotics. For others, the intersection of logistics and robotics was still a far-off notion.

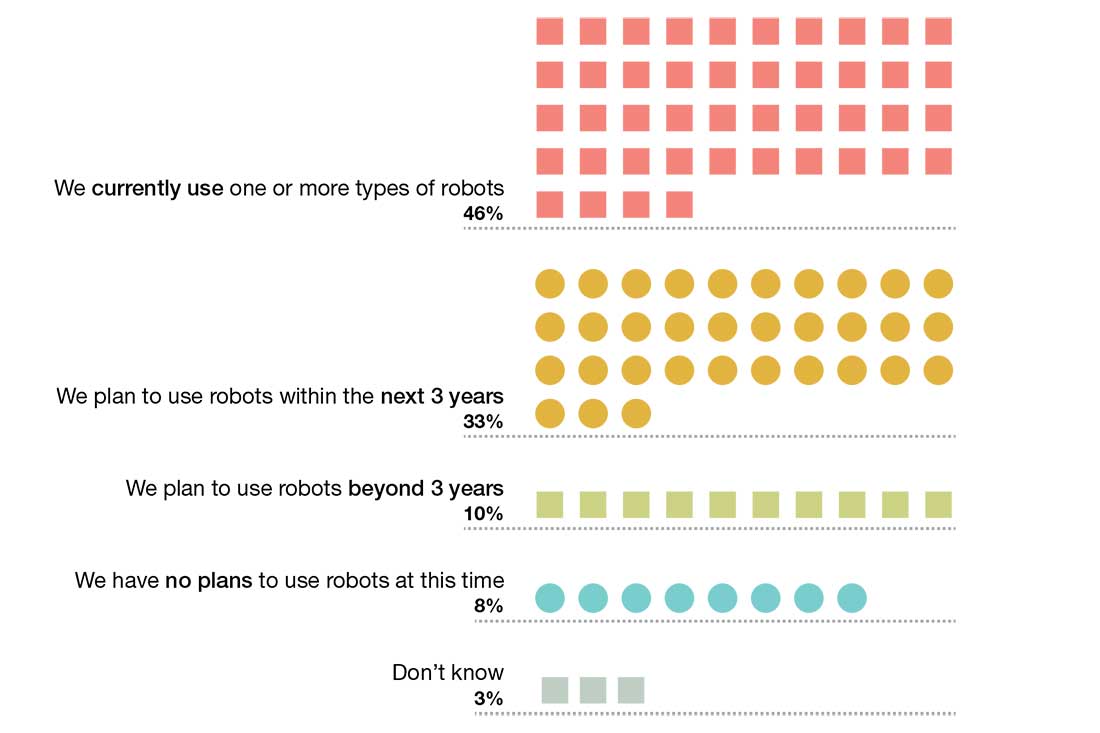

Consider this: When Peerless published the first survey, 40% of respondents said they had no plans to use robots in the future. Only 23% of respondents said they were currently using robotics. Fast-forward to 2024 and 46% of companies now have plans to use robots and just 8% have no such plans.

This is a significant jump in a short period of time, and it proves the undeniable value that comes from having robots perform increasingly complex tasks in the DC or warehouse.

Who’s buying robotics?

For this report, subscribers to Logistics Management, Supply Chain Management Review and Modern Materials Handling were surveyed by e-mail between January and February 2024. This year’s 216 respondents are employed at a variety of different organizations, including manufacturing (32%), other non-manufacturing (21%), transportation or warehousing services (15%) and retail trade (14%).

Respondents hold a wide range of positions from corporate management (28%) to logistics director or manager (16%), to plant manager (12%), to material handling director or manager (7%).

Most participants (40%) work for companies that have less than $50 million in annual revenues, with the next largest group (17%) working for organizations with revenues of $2.5 billion or more. The remaining companies have revenues that range from $100 million to $2.49 billion.

Thirty-three percent of respondents are potential buyers or current users of robotic automation systems and/or services, while 13% provide robotic automation consulting and systems integration services, and 7% are sellers of robotic automation systems and/or services.

Intralogistics automation trends

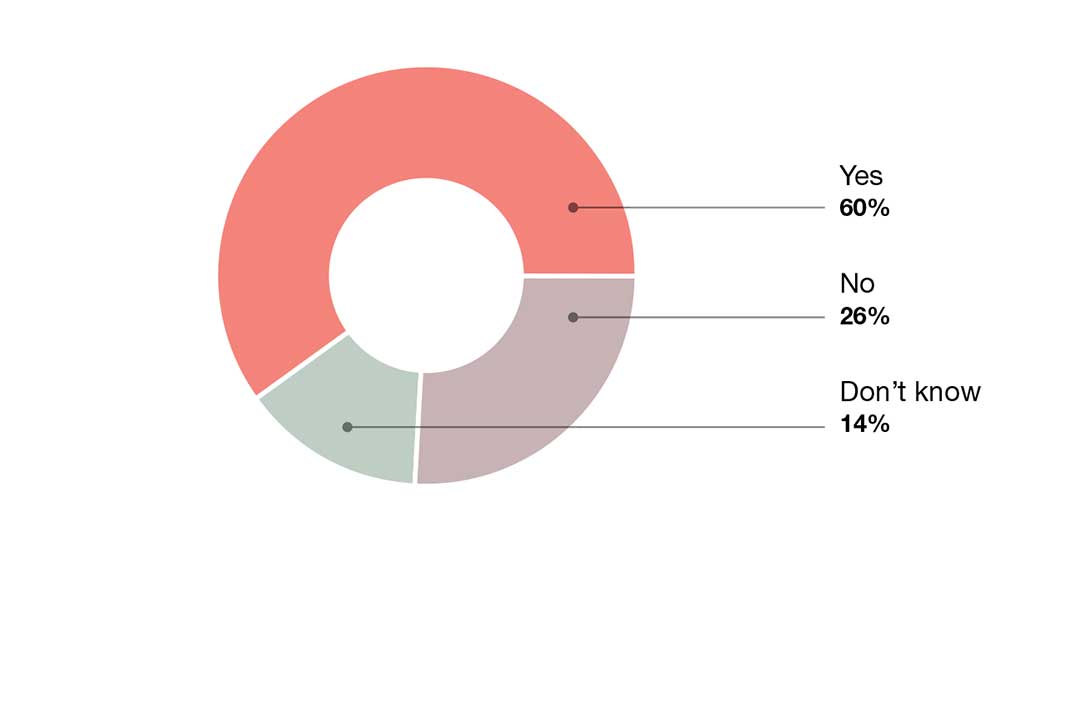

Nearly half (46%) of survey respondents are using one or more types of robots, 33% plan to use robots in the next three years, 10% say they plan to use robots beyond three years, and 8% have no plans to use robots at this time. Most companies (60%) are currently using or considering other types of large-scale intralogistics automation like conveyors, sortation, storage/retrieval or shuttle systems, while 26% are not.

In assessing the “outside factors” that may impact their decision to implement more robotics, 34% expect a significant impact from economic recession; 28% point to labor costs and constraints; 24% expect significant impacts from inflation, and 17% expect significant issues related to environmental, social and governance (ESG) issues. A small percentage of respondents expect no impacts from any of these issues.

Fourteen percent of companies say labor costs and constraints will significantly increase their investment in robotics. Nine percent say inflation will significantly increase their investment plans and a similar percentage see economic recession as a driving force behind their robotics investments over the next two years.

Gearing up for robotics implementation

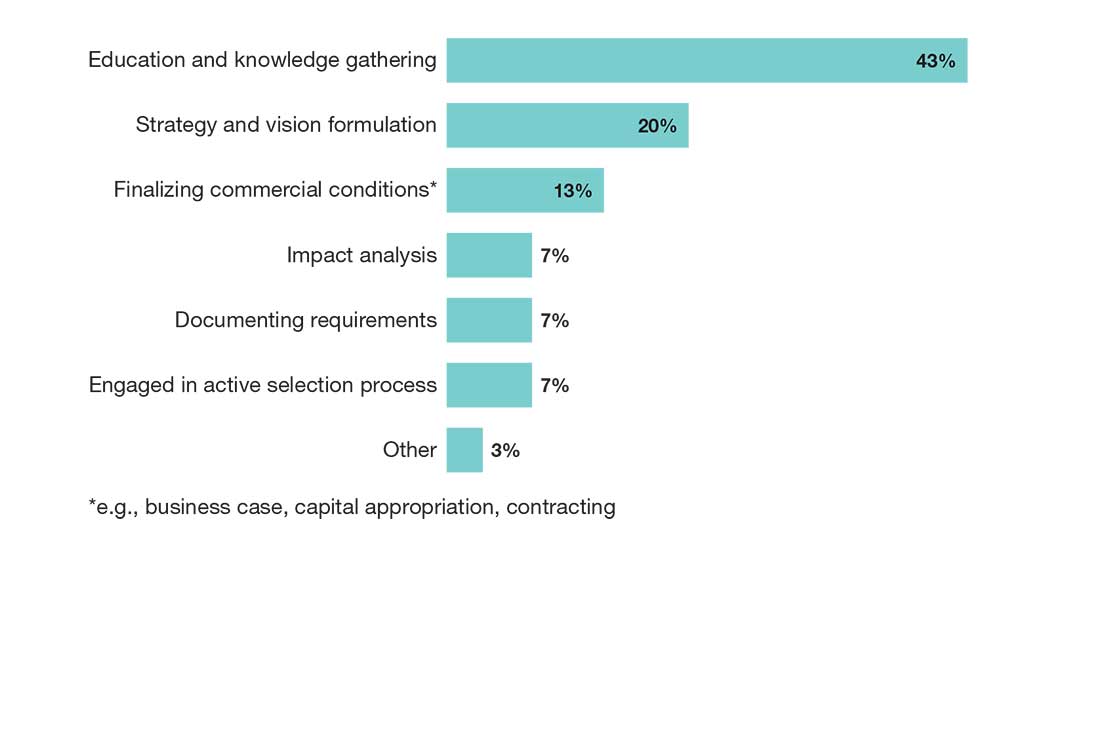

Asked to describe the current state of their organizations’ warehouse robotics initiatives, 43% of companies are in the education and knowledge gathering stage; 20% are in the strategy and vision formulation stage; and 13% are finalizing their business cases and capital appropriation. Others are in the process of impact analysis (7%), documenting requirements (7%) or are engaged in the active selection process (7%).

In ranking the top three motivating factors for pursuing a robotics strategy, companies are most interested in addressing labor shortages and availability constraints, reducing labor costs and improving labor productivity.

Of the respondents that want to implement robots in the future, most (63%) plan to work with robotics vendors—up from 39% last year, industry peers (56%, versus 29% last year) and materials handling suppliers (33%). Others turn to industry trade associations (30%), internal domain experts (22%), systems integrations (15%) or industry analysts/advisory firms (15%) for help in this area.

Looking for improvement

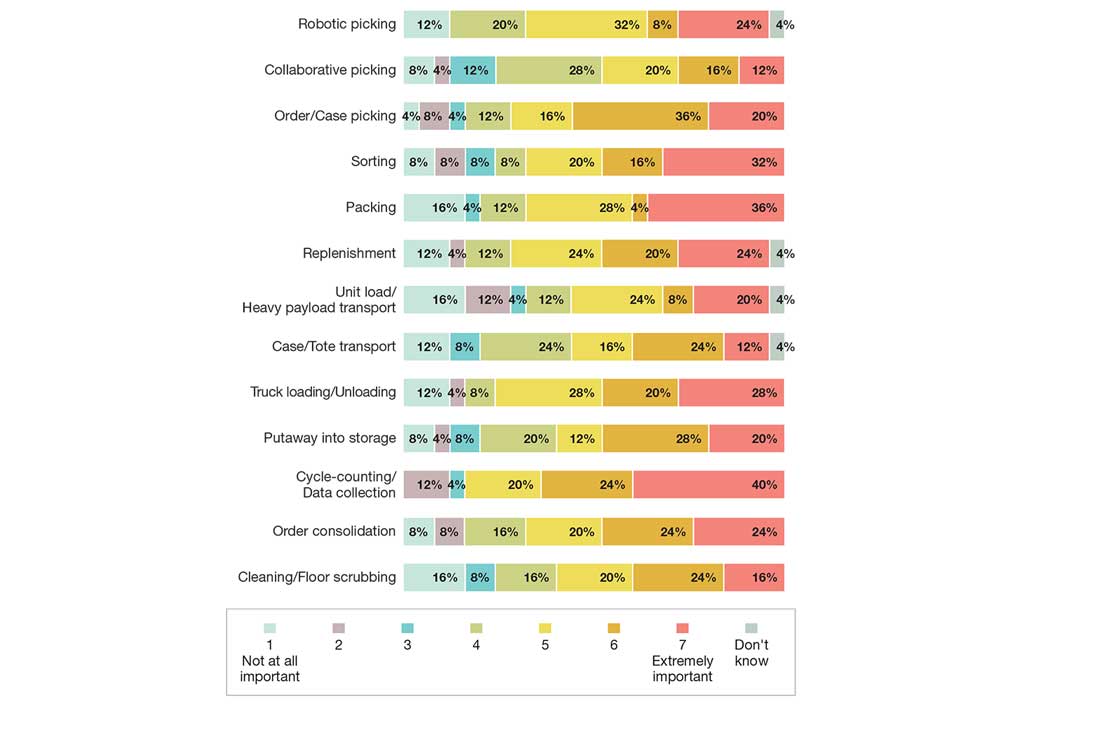

The modern warehouse is a complex animal where cycle counting and data collection (40%), packing processes (36%), sorting (32%) and truck loading and unloading (28%) are all processes that are ripe for improvement. Twenty-four percent of companies see robotic picking as being extremely important, while 24% want to improve replenishment processes, and an equal number want better than 24% order consolidation processes.

The top priorities for robotics right now include robotic picking (32%), cycle-counting and data collection (32%), sorting (28%), replenishment (28%), and truck loading and unloading (28%). Other companies want to use robotics for order/case picking (24%), packing (24%), unit load/heavy payload transport (20%) and order consolidation (20%).

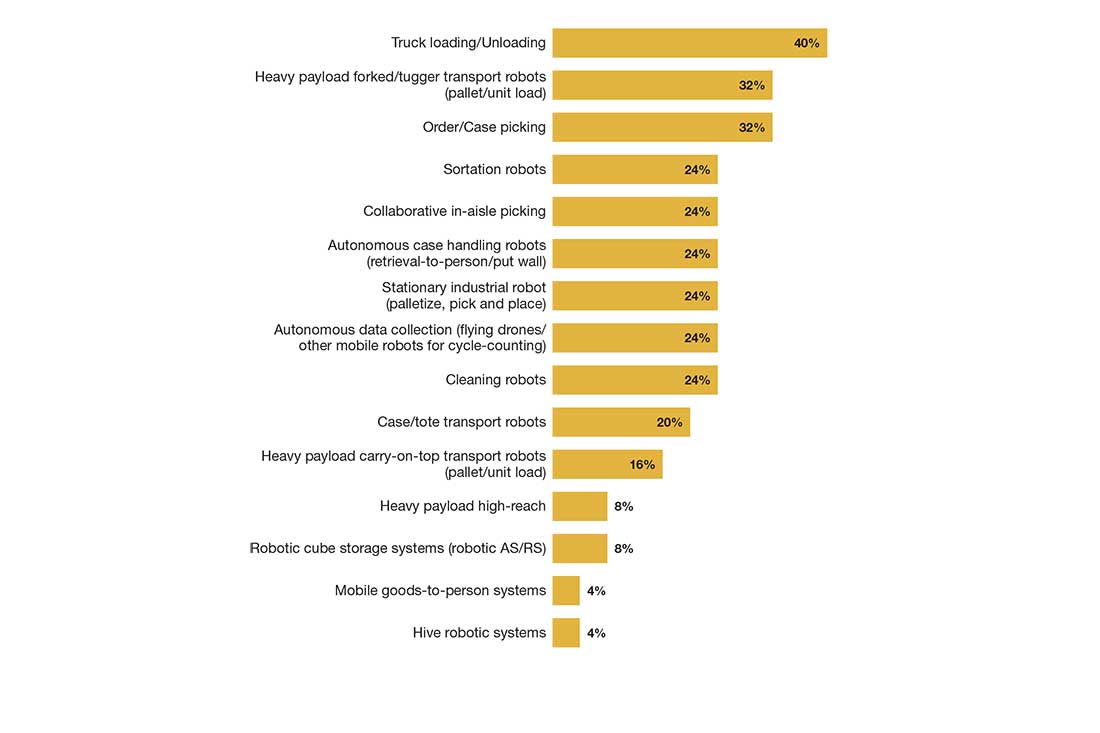

Looking out over the next three years, 40% of companies hope to use robotics for truck loading and unloading, 32% for heavy payload forked/tugger transport robots, 32% for order/case picking and 24% for sortation. Other types of robotics of interest include collaborative in-aisle picking systems (24%), autonomous case handling robots (24%) and stationary industrial robots (24%).

Making the investment

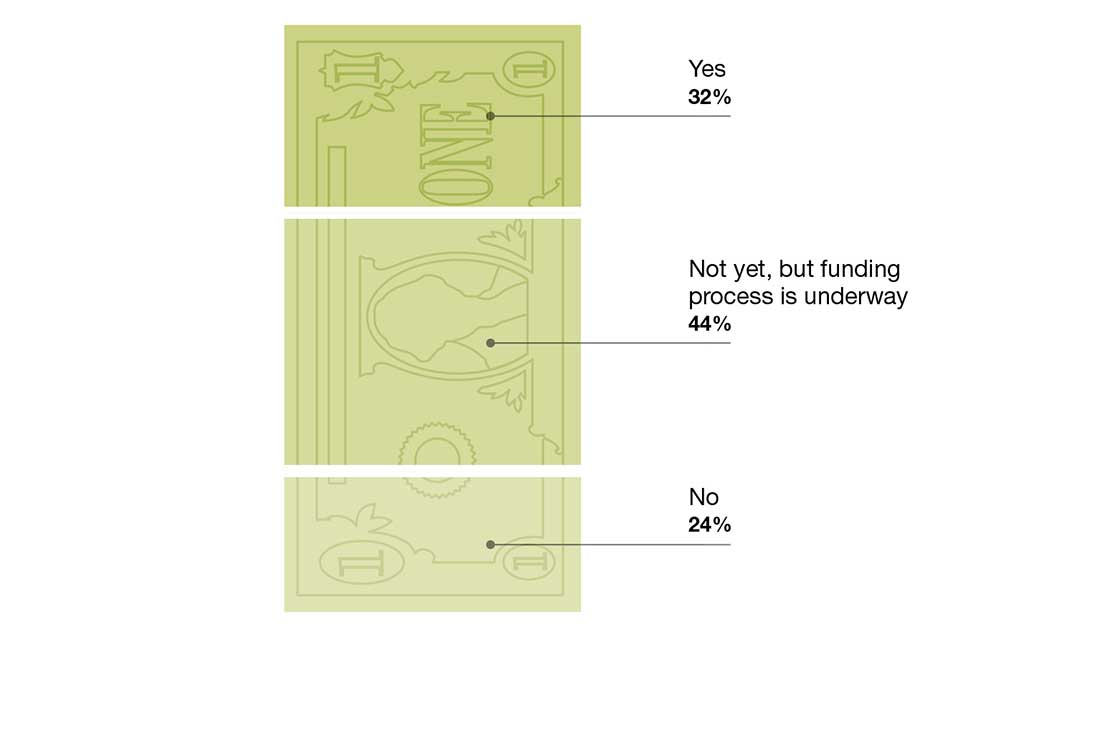

Organizations are investing in warehouse robotics for a number of different reasons, with the top three being to improve labor productivity, reduce labor costs and help address labor shortages and availability constraints. Nearly one-third (32%) of companies say they already have the funding in place for these initiatives (versus 14% in 2023), while 44% lack the funding but are going ahead with the process anyway.

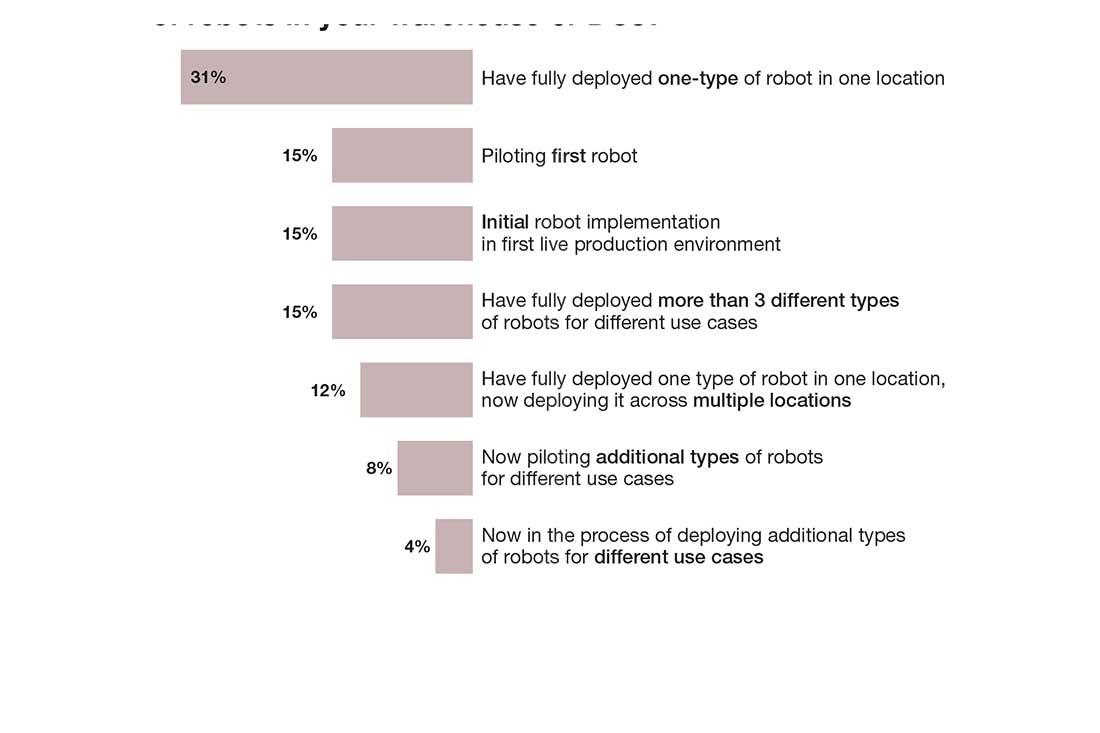

Of the companies currently using robotics, 31% of companies have fully deployed one type of robot in one location (compared to 22% last year), while 15% are piloting their first robot (6% last year), 15% say they have an initial robot implementation in the first live production environment and 15% have fully deployed more than three different types of robots for different use cases.

If forced to make a choice, most companies (58%) say labor availability constraints would be their most important motivation when considering robotics, while 38% say labor costs are the primary driver.

Take robotic fleets to the next level

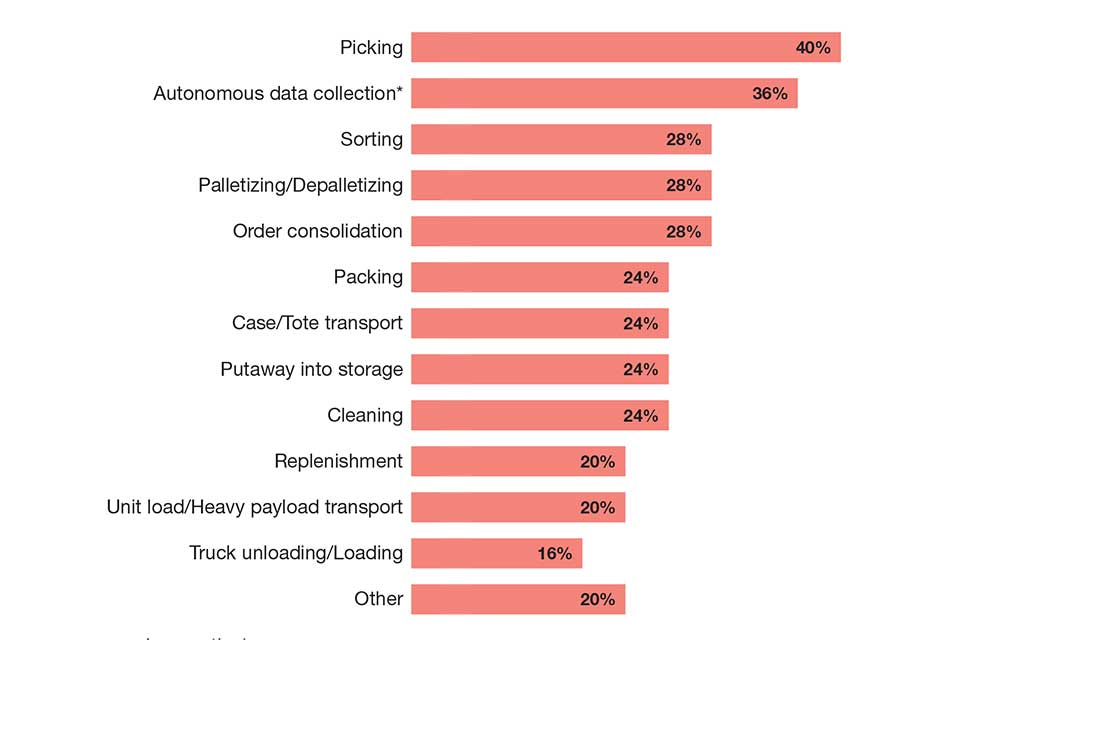

The most popular use cases for robotics today are picking (40%), autonomous data collection (36%), sorting (28%) and palletizing/depalletizing (28%). Twenty-eight percent of companies are using robotics for order consolidation, 24% for packing (down from 35% last year), 24% for case/tote transport and 24% for put-away into storage.

The most popular robotics include stationary industrial robots (36%), robotic picking systems (32%), cleaning robots (28%) and sortation robots (24%). Case/tote transport robots are currently in use at 20% of companies, while 12% rely on heavy payload carry-on-top transport robots and 12% use mobile goods-to-person systems. Other types of robotics currently in use include autonomous case-handling robots (12%) and robotic cube storage systems (12%).

Most survey respondents (71%) plan to expand their robotic fleet in the next two years. Twenty-five anticipate a significant increase in fleet size across multiple facilities and 21% expect a significant fleet size increase within a single facility during that period.

For the majority of companies (46%), picking is the next use case priority for robots (up from 38% last year). Other processes that respondents want to automate with robotics include sorting, packing, truck loading/unloading, put-away into storage, case/tote transport, replenishment and palletizing/depalletizing.

Over the next two to five years, companies say they’ll be most interested in sortation robots (33%), robotics picking systems (33%), robotic cube storage systems (29%) and case/tote transport robots (25%).

Twenty-one percent will consider heavy payload forker/tugger transport robots, another 21% say they’ll consider autonomous case-handling robots and an equal percentage have set their sights on stationary industrial robots.

Using robots to hit business goals

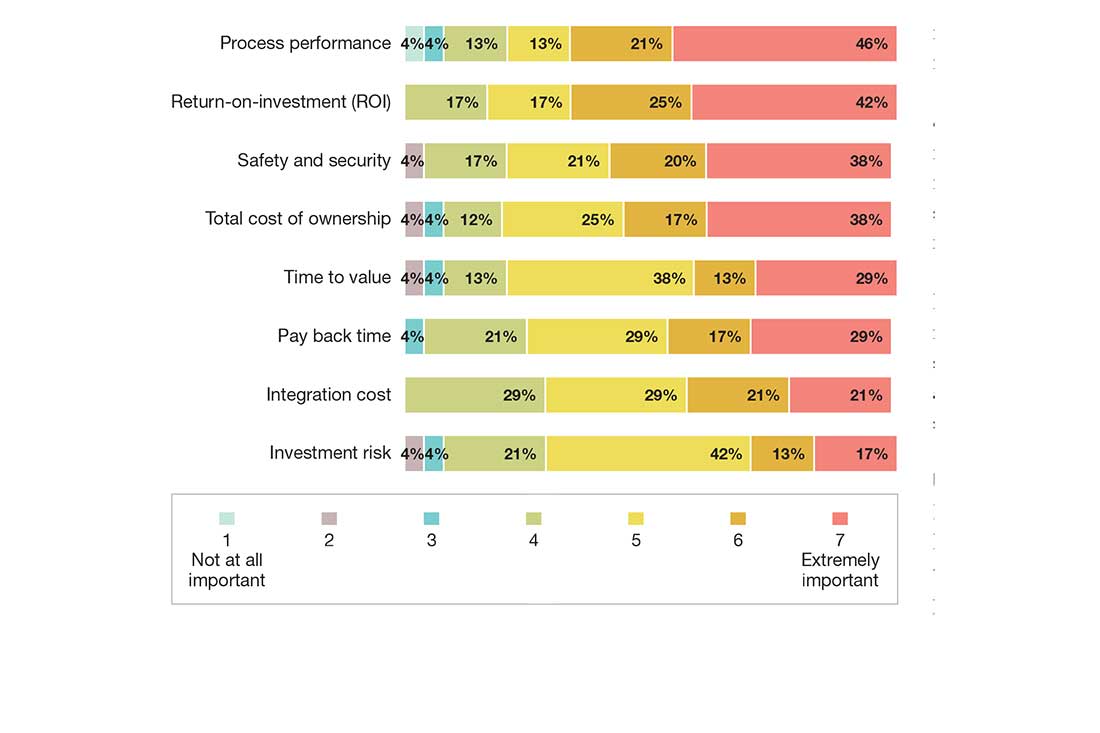

In the increasingly competitive logistics landscape, automation can be a strategic step toward unlocking efficiency, profitability and a competitive edge. When selecting robotics, companies use process performance (46%), return on investment (42%), safety and security (38%) and total cost of ownership (38%) as their key criteria. Other important metrics that factor into buying decisions include time to value (29%), payback time (29%), integration cost (21%) and investment risk (21%).

So how well are today’s intralogistics robotics meeting these expectations? According to the survey, nearly all (91%) of companies had their time-to-value objectives met or exceeded; 88% were satisfied with the integration costs and 83% had their process performance objectives met or exceeded. Finally, 79% of respondents say the total cost of ownership expectations were either met or exceeded for their robotics investments.

The rise of e-commerce, ever-increasing customer expectations and the persistent warehouse worker shortage are all putting pressure on warehouses to work faster, improve throughput, be more accurate and operate more efficiently. And while there’s no doubt that human workers are irreplaceable, this year’s intralogistics survey proves that robots are emerging as powerful tools that help fulfillment centers boost performance and do more with less.

Article topics

Related Slideshow

Related Robotics News