If Modern’s 2018 “Usage and Implementation of Warehouse and DC Automation Solutions” reader survey is any indication, conventional fulfillment equipment is rapidly giving way to an infusion of automated conveyor and sortation systems; goods-to-person picking solutions; and storage solutions, to name just a few of the innovations making their way into the modern-day warehouse.

Conducted by Peerless Research Group on behalf of Modern Materials Handling to assess usage and purchase intentions for automation systems and solutions used in warehouse and distribution center operations, the survey explored the factors and features considered important when evaluating automation systems and solutions for possible purchase.

The survey also looked at how warehouse processes are being automated, operational areas that companies are looking to improve over the next two years; and overall usage and implementation/upgrade plans for equipment used in warehouses and DCs.

The e-mail survey questionnaire was sent to readers of Modern Materials Handling in January of 2018, yielding 191 qualified respondents. Survey respondents are all personally involved in the purchase decision process for materials handling solutions for their companies and work in the food, beverage and tobacco; automotive and transportation; chemicals/pharmaceuticals; and fabricated metals industries (among others).

The e-mail survey questionnaire was sent to readers of Modern Materials Handling in January of 2018, yielding 191 qualified respondents. Survey respondents are all personally involved in the purchase decision process for materials handling solutions for their companies and work in the food, beverage and tobacco; automotive and transportation; chemicals/pharmaceuticals; and fabricated metals industries (among others).

The companies have an average of 752 employees, with 42% having 100 to 499 employees and 38% having less than 100 workers. Twenty-two percent of firms had either less than $10 million or $10 million to $49.9 million in annual revenues, while 11% had either $50 million to $99.9 million or more than $5 billion in revenues.

Price is becoming less of an issue

As the picture of the completely connected warehouse continues to come into focus, that vision is supported by a new crop of hardware and software solutions that support and/or work in tandem with today’s workforce. And as human capital becomes more difficult to recruit and retain, these automated solutions are helping companies manage the labor challenge while maintaining productivity and profitability.

This year, companies expect to spend more on materials handling equipment and solutions than they did last year, with the total average expected spend to be $1.25 million, versus $1.17 million for 2017. And, 34% of firms will spend less than $100,000; 18% say they will spend $100,000 to $499,999; 13% say they will spend $500,000 to $999,999; and 16% want to spend $1 million to $2.49 million. In most cases, companies procure their order fulfillment solutions direct from manufacturers (70%) or from distributors/dealers (60%).

This year, companies expect to spend more on materials handling equipment and solutions than they did last year, with the total average expected spend to be $1.25 million, versus $1.17 million for 2017. And, 34% of firms will spend less than $100,000; 18% say they will spend $100,000 to $499,999; 13% say they will spend $500,000 to $999,999; and 16% want to spend $1 million to $2.49 million. In most cases, companies procure their order fulfillment solutions direct from manufacturers (70%) or from distributors/dealers (60%).

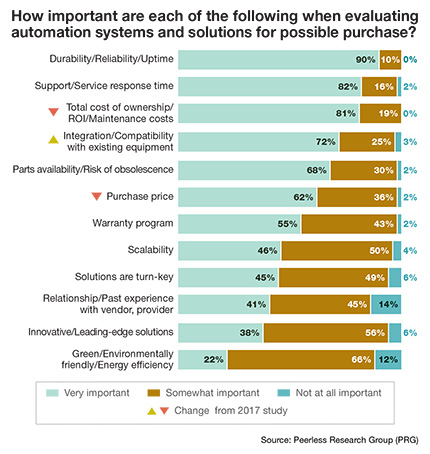

When evaluating automated solutions, most of Modern’s readers (90%) said durability, reliability, and uptime were their top criteria. Other key factors when shopping for new systems include support and response time (82%), with total cost of ownership (TCO), return on investment (ROI), and maintenance costs also playing important roles in the selection process for 81% of respondents. And, 62% say purchase price is important (compared to 71% last year).

Bryan Jensen, chairman and executive vice president at St. Onge Co., says the reduced emphasis on purchase price is an interesting trend that he’s also seeing right now in the market. Automation as a whole has also been considered “forward thinking,” he says, and as such, purchase price tends to make or break the business cases for these investments. “Everyone wants an ROI; they want payback,” says Jensen, who credits the labor shortage with eroding some of the emphasis on payback. “Whether real or imagined, the labor shortage seems to be driving their willingness to invest.”

More specifically, Jensen says firms are likely looking more closely at how they may have to pay $3 to $5 more per hour to maintain current staff levels, bring in flex workers, or fill positions during peak season—an expensive proposition in a world where human capital is becoming scarcer. “If companies weigh it out and see that their [traditional] strategies are going to be more expensive,” he says, “then some will just make the leap to automation.”

The current state of warehouse automation

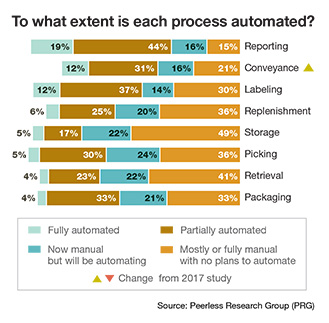

In looking around at the current state of their warehouses, survey respondents said the highest percentage of automation was being used for reporting, where 44% of operations are partially automated, 19% are fully automated, and 16% are planning to automate in the near future. This represents an upward trend over 2017, when 31% were partially automated, 12% were fully automated, and 21% had no plans to automate.

For now, storage and retrieval remain the “least automated” systems in the warehouse, with 49% saying they have no plans to automate storage (and just 5% are fully automated in this area) and 41% saying they aren’t going to automate retrieval (where 4% are now fully automated).

Asked to describe their current order fulfillment operations, 6% of survey respondents say their order fulfillment is fully automated (versus 5% last year); 53% say they have a mix of automated and manual operations (52% last year); and 39% say they are mostly or all manual (down from 41% last year).

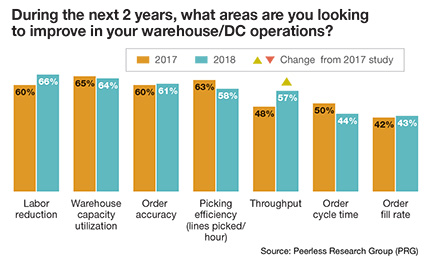

In looking at the areas of the warehouse or DC they’re planning to improve over the next two years, 57% of readers say throughput (versus 48% last year); 66% say labor (60% in 2017); 58% feel picking efficiency should be the biggest target for improvement (versus 63% last year); and 44% have their eyes on order cycle times (50% in 2017).

To manage order fulfilment, 91% of readers are using warehousing and storage (up from 86% last year); 69% use case and mixed case fulfillment (up from 57% last year); 69% currently use full and mixed pallet load fulfillment (up from 59% last year); and 69% use individual pick, pack and ship wholesale distribution fulfillment (up from 64% last year). Those companies that have upgrades planned over the next 24 months intend to use warehousing and storage (38%); case and mixed case (40%); or full and mixed pallet load fulfillment (41%).

What is everyone using?

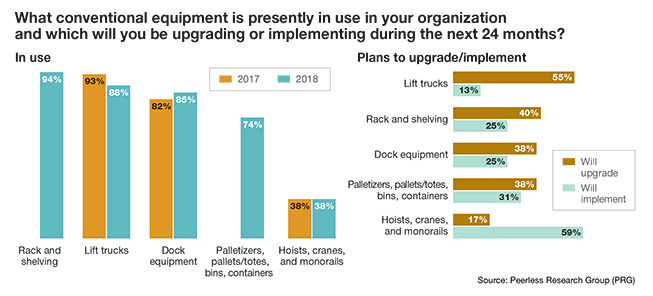

When it comes to conventional equipment, 94% of companies are currently using rack and shelving, while 40% plan to upgrade that equipment in the next two years, while 25% will begin implementing them. Eighty-eight percent are using lift trucks (down from 93% last year), and 55% are planning to upgrade their lift trucks in the next 24 months. Eighty-five percent of respondents rely on dock equipment (up from 82% last year), and 38% will upgrade their dock equipment in the next 24 months. Another 25% of companies plan to implement dock equipment in the next two years.

To position and/or relocate goods within the warehouse, 74% of readers currently use palletizers, pallets/totes, bins and containers. Thirty-eight percent want to upgrade these systems over the next 24 months and 31% will implement these options in the next two years.

Also, 38% of companies are using hoists, cranes, or monorails (the same number as 2017), and 76% of firms want to either upgrade current or implement these solutions in the next two years.

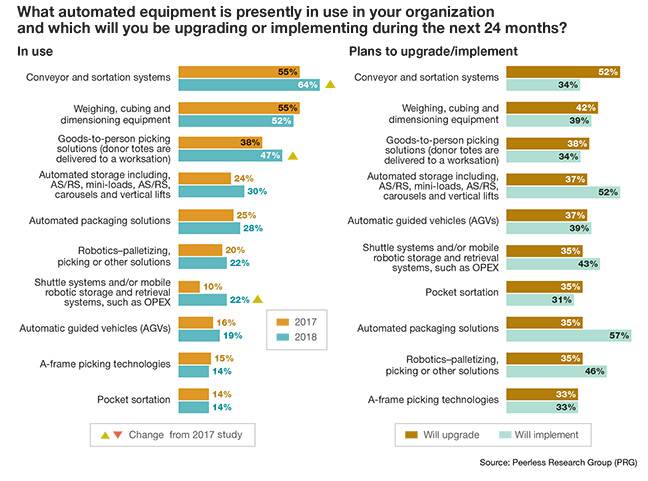

On the automated side of the house, most companies (64%) say they’re using conveyor and sortation systems (versus 55% in 2017), while 52% are using weighing, cubing and dimensioning equipment. And, 86% of respondents will either implement new or upgrade existing conveyor and sortation systems over the next two years, while 81% say the same about their weighing, cubing and dimensioning equipment.

Goods-to-person picking solutions (i.e., donor totes delivered to a workstation) are gaining in popularity, with 47% of respondents using them, up from 38% last year. Right now, 38% of companies will upgrade and 34% will implement such solutions in the next 24 months.

Among the biggest shifts in this year’s survey involved the use of shuttle systems and/or mobile robotic storage and retrieval systems such as OPEX. Twenty-two percent of companies are currently using these systems versus 10% in 2017.

For 2018’s survey, 35% of respondents say they plan to upgrade these solutions and 43% plan to implement them in the next two years. Automated packaging solutions are also getting more traction in the connected warehouse, where 28% of companies use them, 35% want to upgrade their current solutions, and 57% plan to implement such technology over the next two years.

Jensen says he’s also seeing more companies taking an interest in automated shuttle systems, mobile robotic storage and retrieval, and automated packaging. He says vision systems are also “coming into their own” right now due to the cool factor they bring to the table. According to the survey, heads-up display/vision technologies are currently being used by 16% of respondents and are on the radar screen for 56% of firms.

“Even the most automated shuttle system just looks like a bunch of mechanical connections to the average person,” Jensen points out, “but when you get bots and different devices moving around, using vision systems—and literally on their own paths and not using rails—they just show better and look more futuristic.”

Software solutions

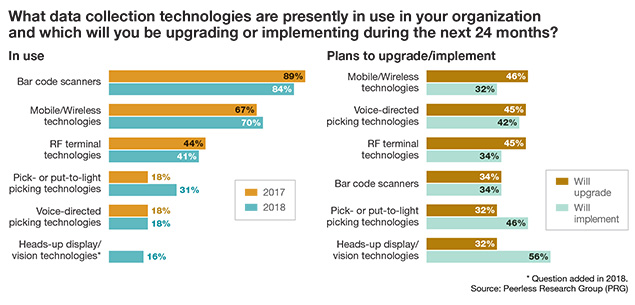

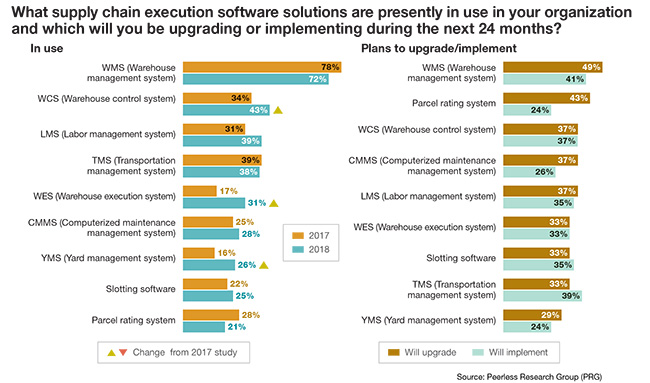

In the warehouse, data collection is largely handled with bar code scanners (used by 84% of companies), mobile/wireless technology (70%), and RF terminal technologies (41%). When asked which supply chain execution software solutions they’re using, 72% said warehouse management systems (WMS); 43% said warehouse control systems (WCS); 39% are using labor management systems (LMS); and 38% rely on transportation management systems (TMS).

The highest percentage of readers (90%) have set their sights on either upgrading or implementing WMS over the next two years. When asked the same question about their supply chain management software solutions, 59% of readers said they’re using enterprise resource planning (ERP), 52% said customer relationship management (CRM), and 45% rely on order management systems (OMS).

As the nation’s labor market challenges continue to persist, and as customers expect faster and more accurate delivery levels, expect the level of warehouse/DC automation to continue to proliferate over the next few years.

Jensen expects goods-to-person, vision, and automated mixed pallet building applications to all rise to the top thanks to the need for higher productivity levels in an era of tough labor constraints. “These types of applications really cover the bases,” he says, “by helping companies manage their storage, productivity and labor pain points.”

Article topics

Latest Material Handling News